Table of Contents

What Is Insurance?

Insurance is a legal agreement between an individual and the insurance company, under which, the insurer promises to provide financial coverage (Sum assured) against contingencies for an amount (premium).

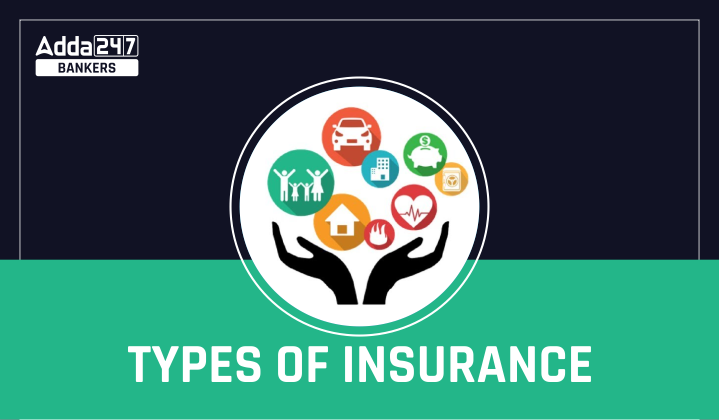

There are 2 types of Insurance in India :-

- General/Non-Life Insurance Policies

- Life Insurance Policies

1. General/Non-Life Insurance Policies :-

General insurance or non-life insurance policy, including automobile and homeowners policies, provide payments depending on the loss from a particular financial event. General insurance is typically defined as any insurance that is not determined to be life insurance.

| Types of General Insurance | |

| Health Insurance |

It helps to meet any unforeseen medical expense. Generally it covers :-

|

| Motor Insurance |

These set of Insurance covers your vehicle ten whether be it your car, bike or commercial vehicle etc. |

| Travel Insurance |

It provides financial protection to you and your loved ones while you are travelling. So that you can travel peacefully. |

| Fire Insurance |

It pays or compensates for the damages to your property or goods due to fire. It also covers for the damages caused to Third party due to fire. |

| Home Insurance | Home insurance provides you coverage for the unforeseen damage or loss caused to the house structure and its content. It provides coverage against human and natural calamities like fire, earthquake, robbery, burglaries, etc. |

2. Life Insurance

Life insurance plans offer coverage against unfortunate events like death or disability of the policyholder. Besides financial protection, there are various types of life insurance policies that allow the policyholders to maximize their savings through regular contributions into different equity and debt fund options.

| Types of Life Insurance | |

|

Term Insurance |

-It is the most basic type of insurance. -It covers you for a specific period. -Your family gets a lump-sum amount in the case of your death. -If, however, you survive the term, no money will be paid to you or your family. |

|

Whole Life Insurance |

-It covers you for a lifetime. – Your family receives a certain sum of money after your death. -They will also be entitled to a bonus that often accrues on such amount. |

|

Endowment Policy |

-Like a term policy, it is also valid for a certain period. -A lump-sum amount will be paid to your family in the event of your death. -Unlike a term plan, you get the maturity proceeds after the term period. |

|

Money-back Policy |

-A certain percentage of the sum assured will be paid to you periodically throughout the term as survival benefit. -After the expiry of the term, you get the balance amount as maturity proceeds. -Your family gets the entire sum assured in case of death during the policy period. This is regardless of the survival benefit payments made. |

|

Unit-linked Insurance Plans (ULIPs) |

-Such products double up as investment tools. -A part of your premium goes towards your insurance cover. -The remaining amount is invested in Debt and Equity. -A lump-sum amount will be paid to your family in the event of your death. |

|

Child Plan |

-This ensures your child’s financial security. -In the event of your death, your child gets a lump-sum amount. -The insurer pays the premium amounts after your death. -Your child will continue to get a certain sum of money at specific intervals. |

|

Pension Plans |

-This helps build your retirement fund. -You can get a regular pension amount after retirement. -In the case of your death, your family can claim the sum assured. |

Tax Benefits

• Life insurance not only ensures the well-being of your family, it also brings tax benefits.

• The amount you pay as premium can be deducted from your total taxable income.

• However, this is subject to a maximum of Rs 1.5 lakh, under Section 80C of the Income Tax Act.

• The premium amount used for tax deduction should not exceed 10% of the sum assured.

Other posts

GA Capsule for SBI Clerk Mains 2025, Dow...

GA Capsule for SBI Clerk Mains 2025, Dow...

The Hindu Review October 2022: Download ...

The Hindu Review October 2022: Download ...

Seating Arrangement Questions for IBPS R...

Seating Arrangement Questions for IBPS R...