Today we have included Data Interpretation, Quadratic Equations and Approximation Questions. You should try to solve these set of questions within 14-15 minutes If you fail to complete it in the stipulated time, then try again with full force. These quantitative aptitude questions are very important from exam point of view like IBPS RRB Exam, IBPS PO and IBPS Clerk.

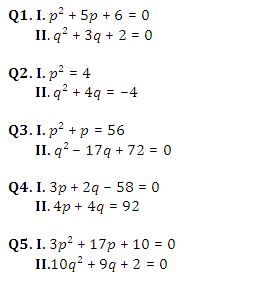

Directions (1-5): For the two given equations I and II.

Give answer (a) if p is greater than q.

Give answer (b) if p is smaller than q.

Give answer (c) if p is equal to q.

Give answer (d) if p is either equal to or greater than q.

Give answer (e) if p is either equal to or smaller than q.

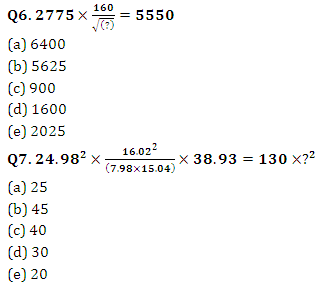

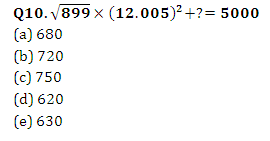

Directions (6-10): Find out the approximate value which should replace the question mark (?) in the following questions. (You are not expected to find out the exact value)

Q8. 71.98% of 1200 + 35.06% of 270 = ?% of 600

(a) 140

(b) 125

(c) 120

(d) 135

(e) 160

Q9. 88.25% of 450 = ?% of 530

(a) 70

(b) 68

(c) 75

(d) 80

(e) 65

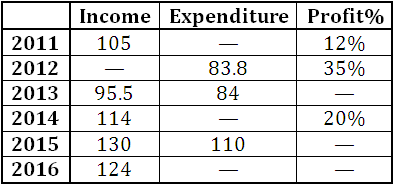

Directions (11-15): Given below is the table showing income, expenditure and profit percentage of company A from 2007-2012.

NOTE: Income and expenditure are in million rupees.

Q11. If percentage increase in profit percent in the year 2016 in comparison to 2012 is 400/7%. Then find the expenditure of the company in 2016.

(a) 85 million

(b) 70 million

(c) 80 million

(d) 75 million

(e) None of these

Q12. Expenditure in 2011 is what percent more or less than the expenditure in 2014? (round off to 2 decimal places)

(a) 2.4%

(b) 1.3%

(c) 1.8%

(d) 2%

(e) 3.2%

Q13. What is average income of the company from the year 2012 to 2014?

(a) 106.4 million

(b) 107 million

(c) 105.45 million

(d) 107.54million

(e) None of these

Q14. Find the ratio of income of the company in 2012 to its expenditure in 2011.

(a) 2: 5

(b) 5: 4

(c) 17: 16

(d) 18: 17

(e) None of these

Q15. If expenditure was increased by 25% in the year 2011 in comparison to previous year, and profit percentage in the previous year was 25% less than the profit percentage in 2011 then find the income in 2010.

Simplification Questions For Bank Exams ...

Simplification Questions For Bank Exams ...

Quantity Comparison Questions for Bank E...

Quantity Comparison Questions for Bank E...

Mixture & Alligation Questions for B...

Mixture & Alligation Questions for B...